Labour in the Construction Sector: Its Image, Young Workers, and the Shortage of Labour

Labour in the Construction Sector: Its Image, Young Workers, and the Shortage of Labour

EUROCONSTRUCT. Briefing on European construction December 2024

EUROCONSTRUCT. Briefing on European construction December 2024

The construction sector faces critical challenges, from labour shortages and demographic shifts to the declining appeal of the industry among young workers. Recent years have seen significant fluctuations, driven by state incentives and their eventual phase-out, leading to a resurgence of irregular employment.

One of the major issues in economic debates concerns the significant growth in employment compared to the moderate growth in GDP. Responses to this phenomenon, which is not exclusive to the construction sector, nor to Italy but also Europe, can be identified in the following aspects: employment growth is concentrated in some low-value-added service activities (e.g., tourism), thus contributing little to economic growth; since it is difficult today to find workers, companies tend to “hold on to” them, leading to weaker layoffs compared to the past, even in struggling sectors; the most crucial factor concerns wage levels and their capacity to keep up with inflation. The issue of wage levels is particularly significant in Italy, which ranks among the lowest in Europe in comparative terms.

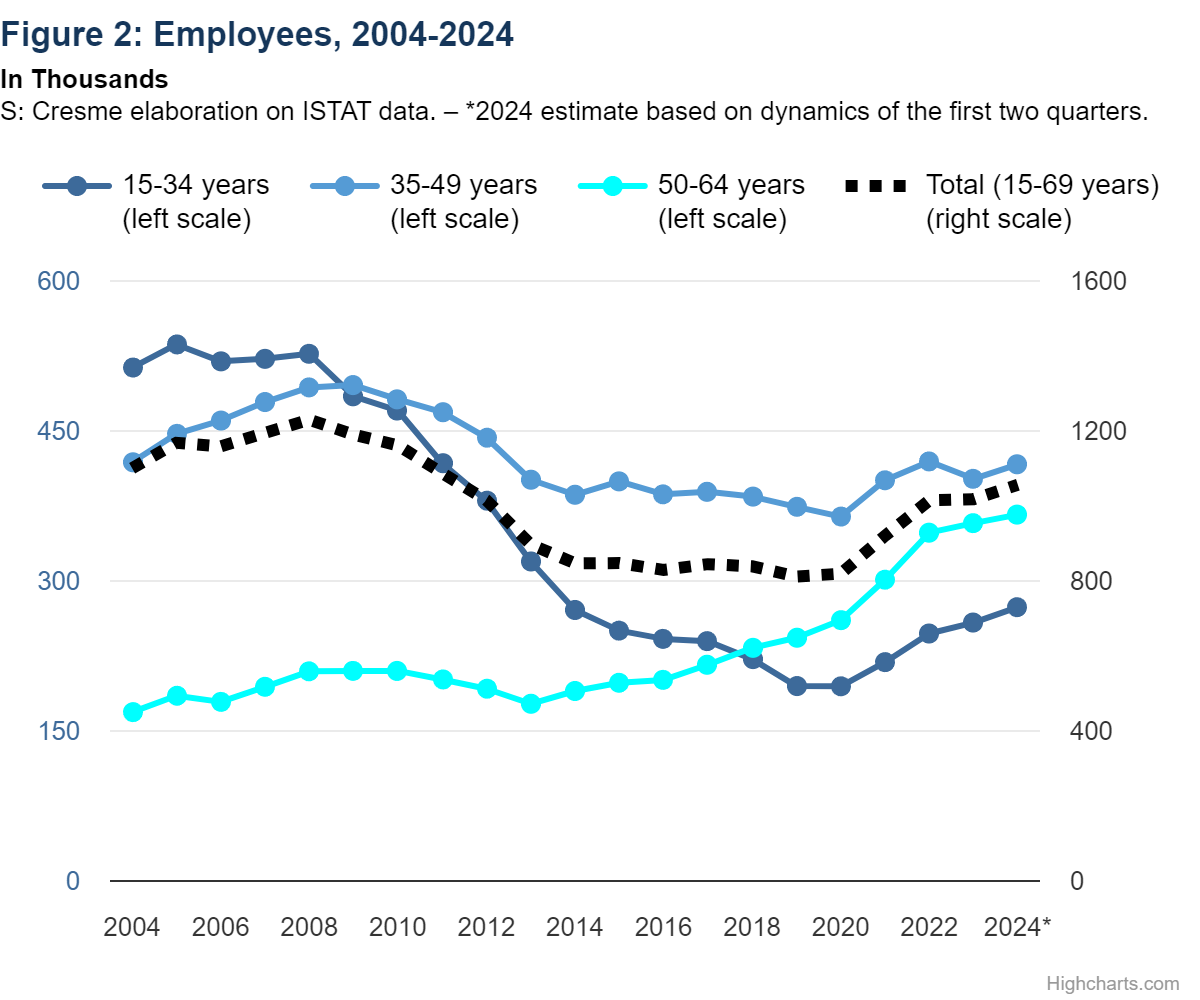

The construction sector has played a key role in employment growth in recent years. Following the robust growth observed in 2021-2022, driven by state incentives for building renovation, the construction sector began to slow down in 2023. The gradual phasing out of incentive policies, such as the “Superbonus 110%”, had a significant impact. According to Labour Force Survey data, the sector lost almost 20,000 workers in 2023 (-1.3%), halting the positive trend of previous years. In contrast, other sectors, such as services (+2.4%) and industry (+2.2%), continued their stable growth. However, in the second quarter of 2024, the sector showed a substantial recovery in employment (+4.5%), outperforming the overall employment growth in the national economy (+1.4%) and the stagnation in industry.

The labour market statistics outlined require particular attention for several reasons. Firstly, official statistics often diverge: during 2021-2022, incentives led to a convergence between National Accounting estimates (which include irregular labour) and Labour Force Survey data, thanks to the need to formalise employment relationships to access tax benefits. In 2021, the discrepancy was approximately 192,000 units (1.623 million employed according to National Accounts versus 1.431 million according to Labour Force Surveys), while in 2022, it was around 182,000 units (1.733 million versus 1.551 million). This dynamic highlighted the significant emergence of undeclared work, driven by strong sector growth and incentives that pushed companies towards regularisation. In 2023, however, the progressive conclusion of incentives triggered a reversal, with a return to undeclared work and a gap of 224,000 units between the two sources, the largest disparity since 2020, signalling a resurgence of irregular employment. This increase in irregular labour underscores the negative impact of reducing incentives and confirms the construction sector’s vulnerability to undeclared work in the absence of structural countermeasures.

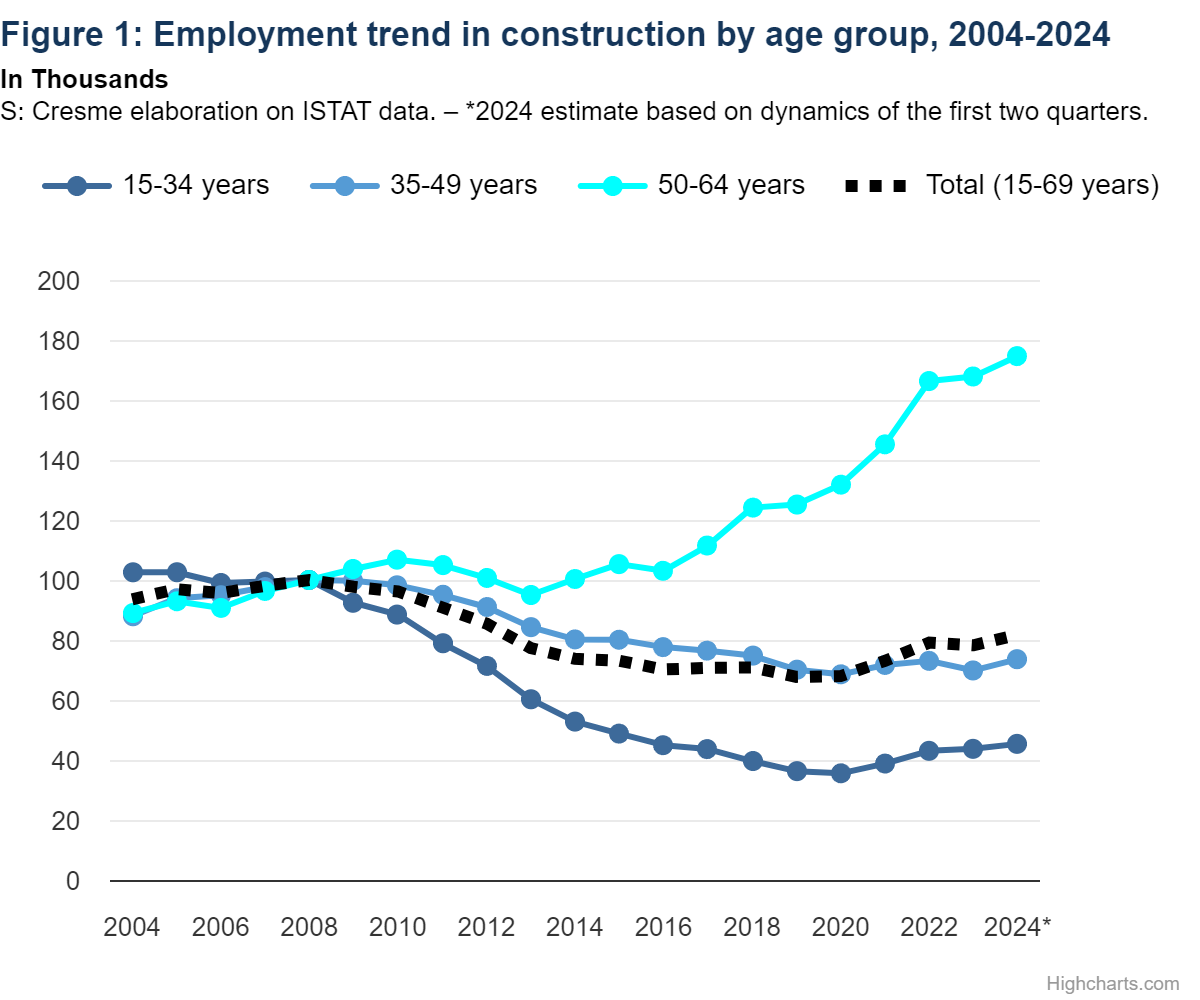

Structural factors also play a role in explaining the divergent dynamics between employment and investments in construction. These include improvements in productive efficiency or the automation of certain activities (where employment declines while investments increase) or the predominance of maintenance and renovation projects, which are more labour-intensive. Additionally, the labour market dynamics are strongly influenced by the age composition of the workforce. This analysis highlights the diminishing appeal of the sector among younger workers. However, recent years suggest a potential shift.

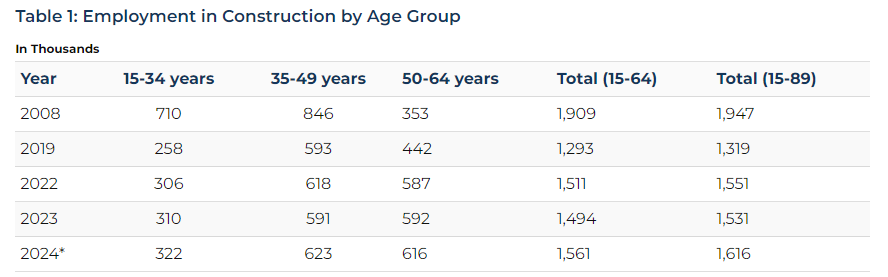

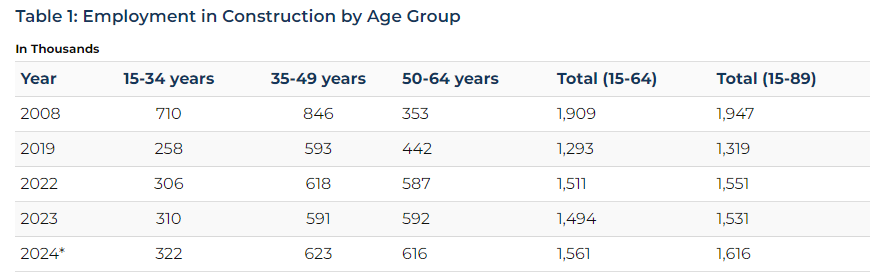

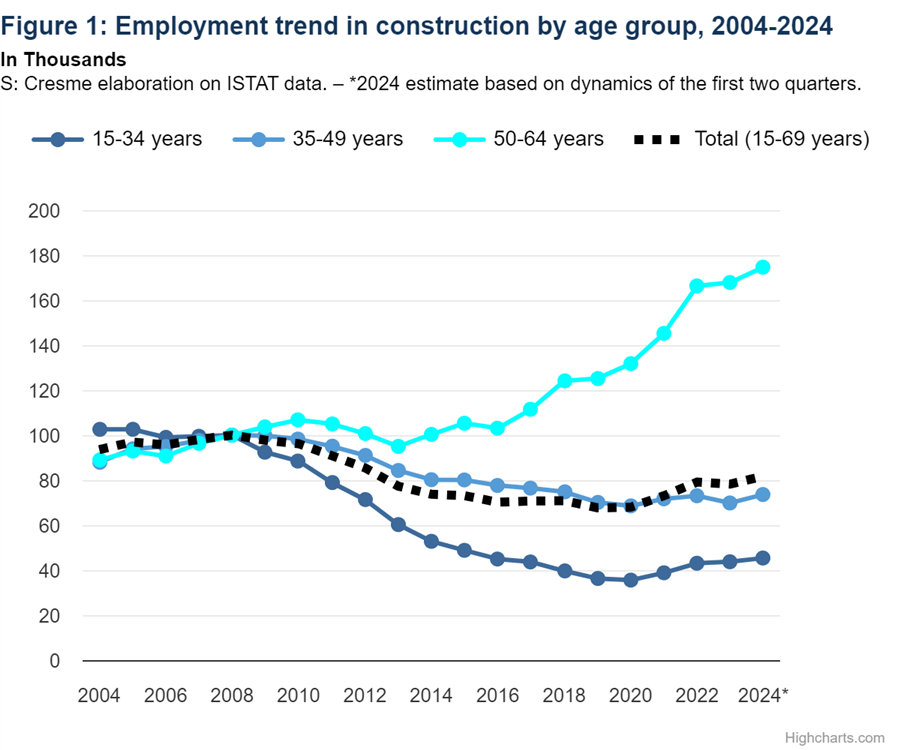

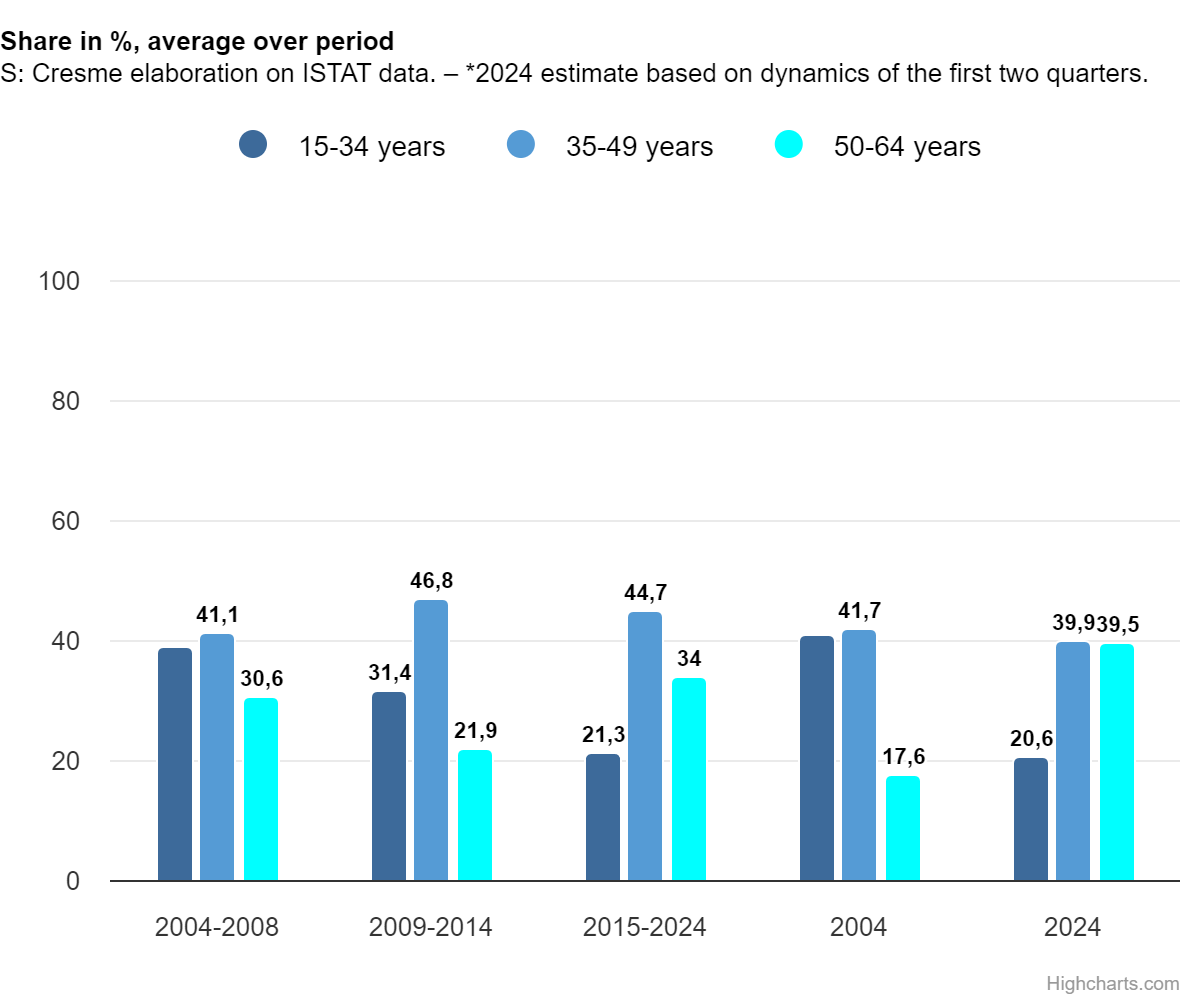

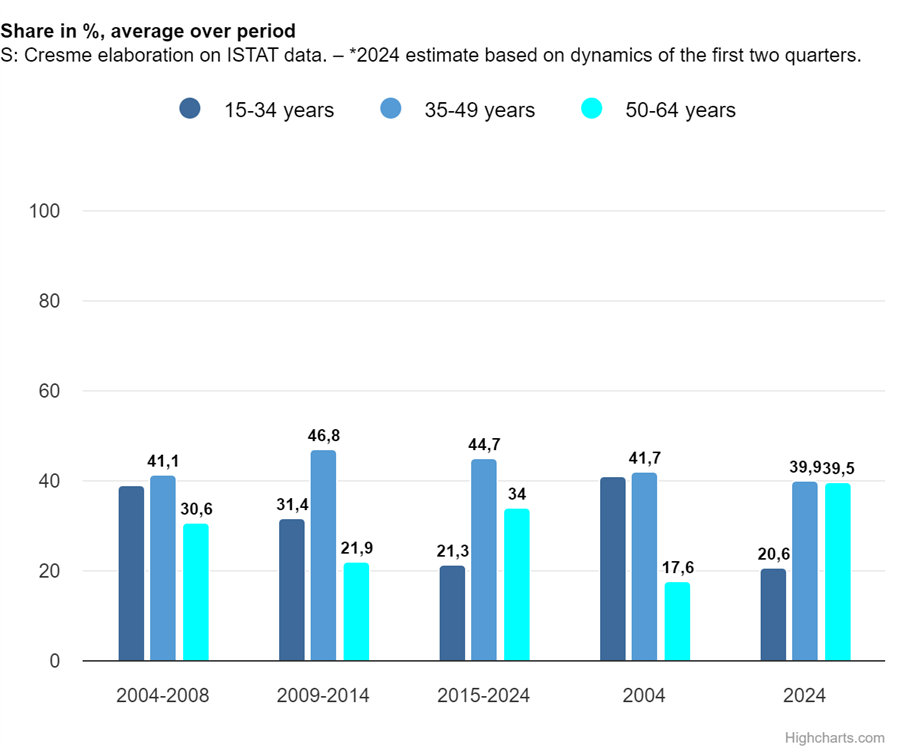

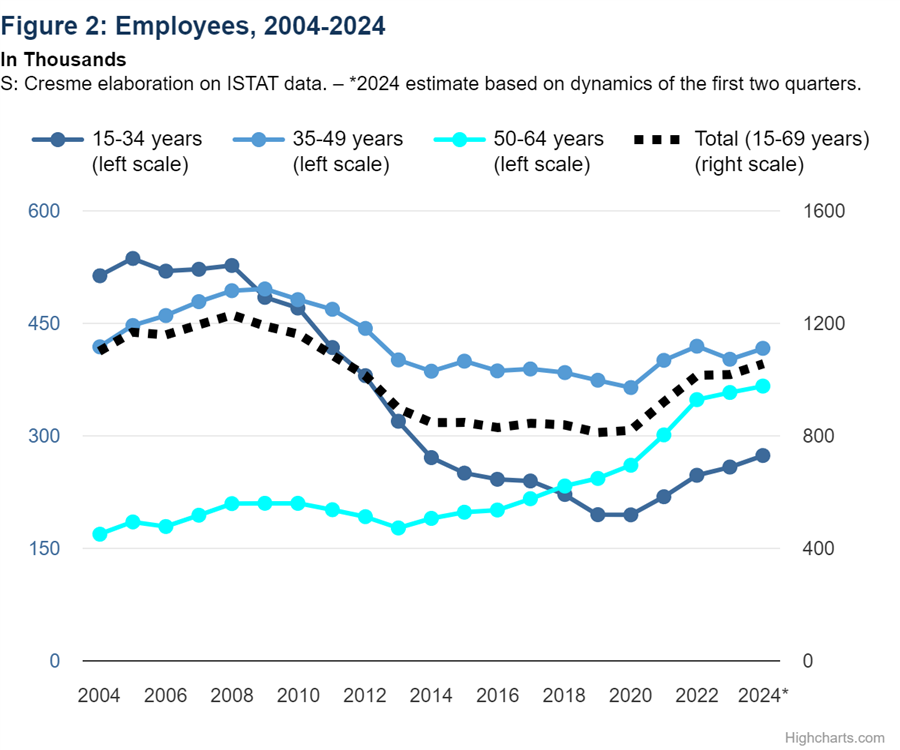

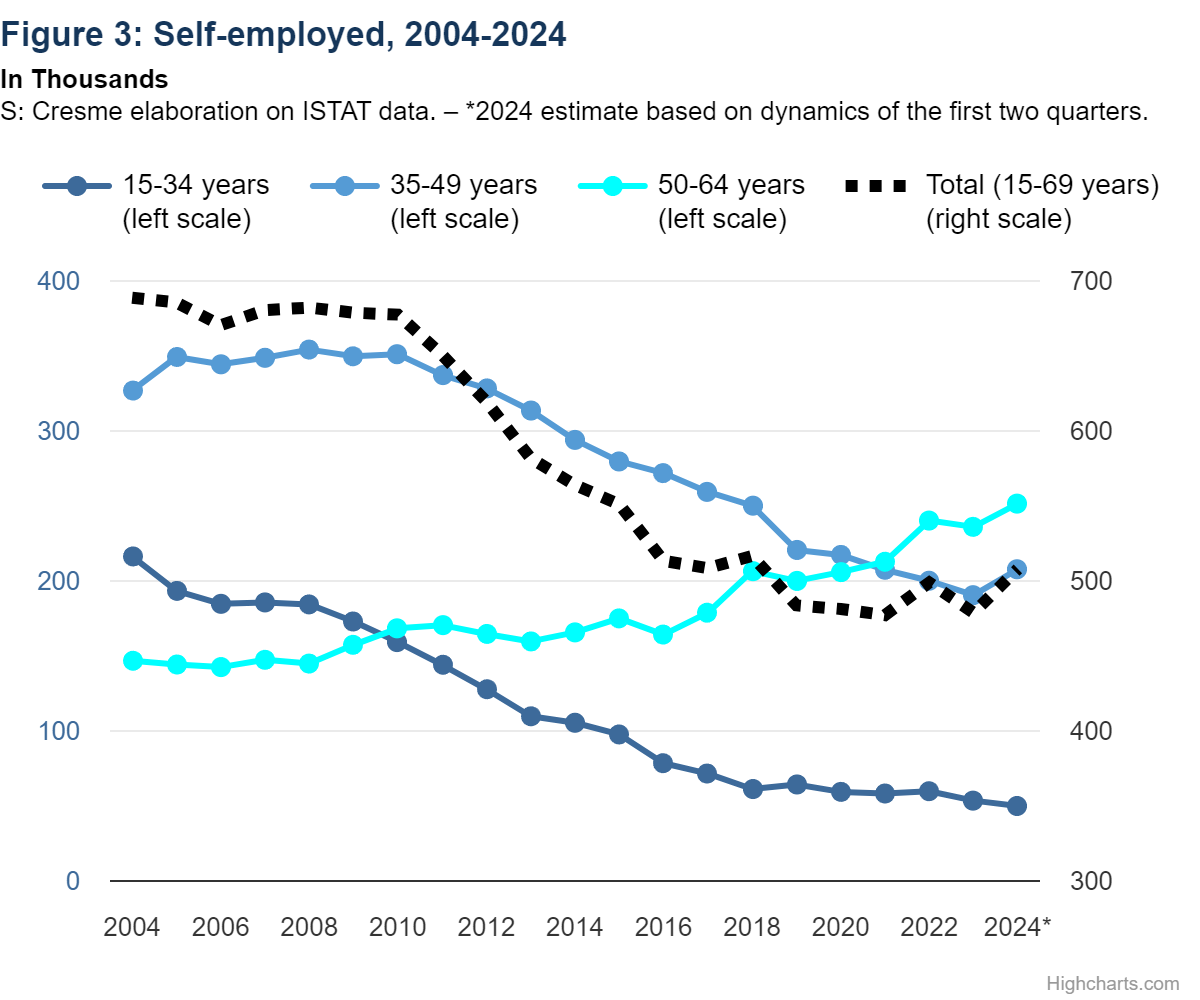

In 2004, workers under 35 accounted for nearly 41% of employment in construction, the same share as those aged 35-49, while less than 18% were over 50. Over the past two decades, younger workers have steadily exited the sector, reaching their lowest level in 2020 (below 20%). However, the share of workers under 50 has not increased, dropping to 45% in 2020 from 49% in 2016. Conversely, the share of older workers (over 50) has doubled from 18% in 2004 to 36% in 2020. Recently, from 2021 to 2024, there has been a renewed interest among younger workers, whose share has risen to 21% of the total. Meanwhile, the 35-49 age group has dropped below 40%, and older workers have reached their highest level of around 40%. Notably, during this period, the share of workers aged 65 and older has increased, from less than 2% in 2004 to 3.4% in 2024. The recent growth in young workers has been concentrated among employees, who grew by 41% between 2020 and 2024, while young self-employed workers decreased by 16%. Similarly, the number of self-employed workers aged 35-49 declined by 4%, while employees in the same age group grew by 14%. Among older workers, employment expanded across the board, with a 41% increase in employees and a 22% rise in self-employed workers between 2020 and 2024.

Educational attainment. Data on job positions in construction firms reveal general growth between 2018 and 2022 among both self-employed and employed workers. However, some vulnerabilities are evident, particularly in the educational attainment of self-employed workers. While the number of self-employed workers grew by 8,544 during this period, almost 12,000 workers exited the sector, all with very low education levels: 8,100 with no education or only primary education, 2,100 with lower secondary education, and 1,300 with vocational qualifications. Conversely, the largest contribution to growth among self-employed workers came from those with secondary or post-secondary diplomas. Among employees, the most significant growth was observed among workers with lower secondary education (+92,000), followed by those with upper secondary education (+70,000).

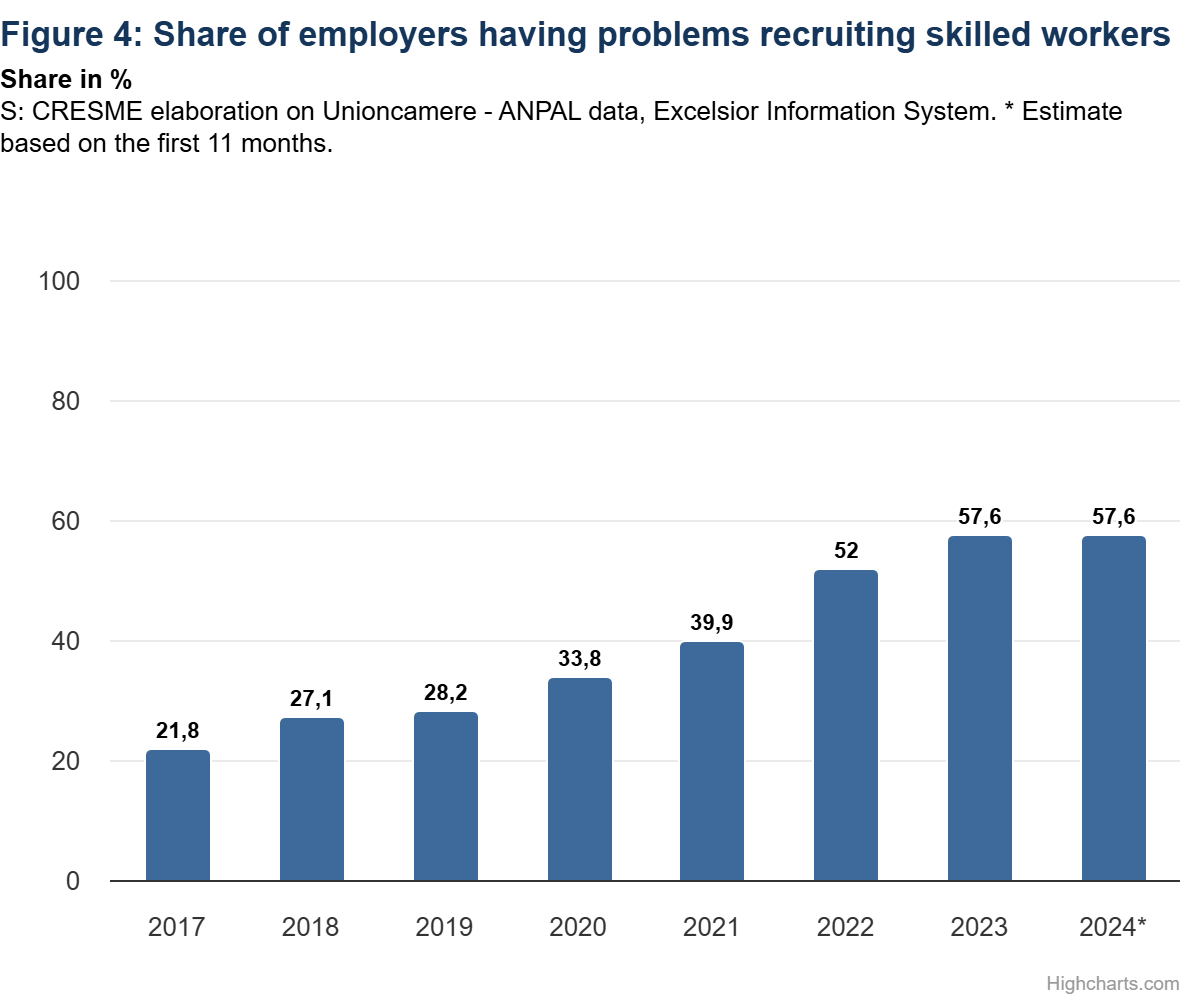

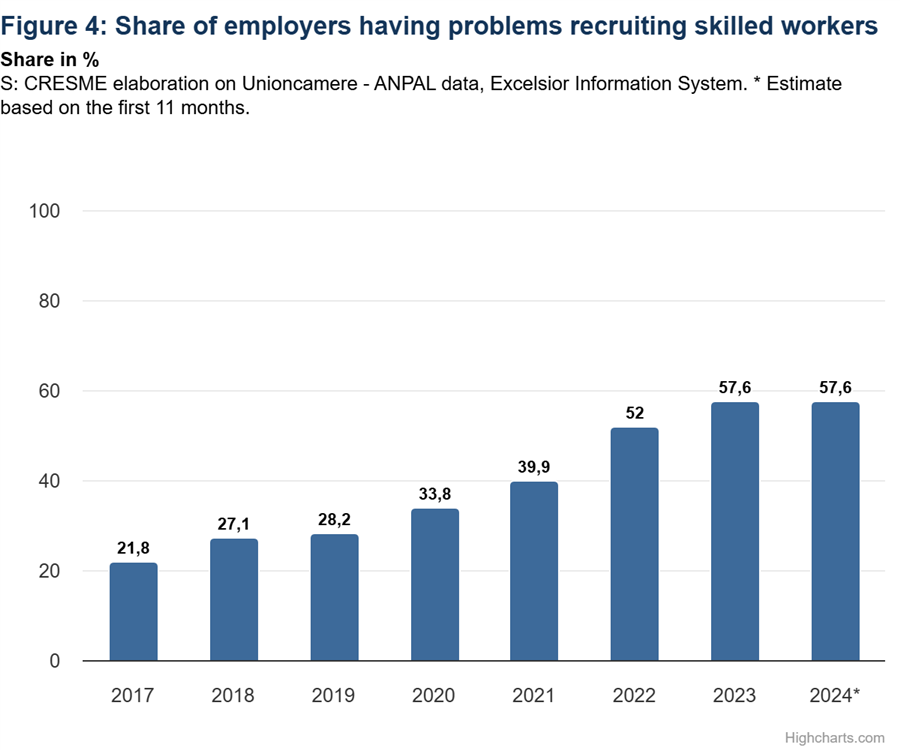

Future hiring trends. The demand for new hires in the construction sector, as surveyed by Unioncamere, has shown a growing trend from 2017 to 2023, interrupted only by the pandemic. Hires increased from over 358,000 in 2017 to nearly 250,000 in 2023, with an estimated 554,000 hires projected based on the first 11 months of the current year. Alongside this growth, the difficulty in finding workers has risen sharply, from less than 22% in 2017 to nearly 58% in recent years. This challenge has been attributed primarily to a reduced number of candidates (58%-61% in the last two years) rather than a lack of qualifications, which was more prominent in earlier years.

The construction sector faces pivotal challenges and opportunities as it navigates a period of modernisation. Persistent difficulties in attracting young workers and the growing mismatch between labour supply and demand underscore the need for targeted policies. Education and structured employment contracts are emerging as critical levers for aligning workforce capabilities with market needs. Furthermore, addressing vulnerabilities such as irregular labour and demographic imbalances is essential. These measures, combined with sustained innovation, are fundamental to ensuring the sector’s resilience and competitiveness in the evolving economic landscape.

Texten är skriven av Antonella Stemperini, analytiker på CRESME Ricerche. CRESME är Italiens representant i det europeiska analysnätverket EUROCONSTRUCT.

Läs mer om Euroconstruct här eller ta kontakt med oss om du är intresserad av bygg- och anläggningsprognoser för de europeiska marknaderna.