SWITCH SECTION

SWITCH SECTION

Tightrope walk to recovery: UK construction still faces post-election hurdles

Tightrope walk to recovery: UK construction still faces post-election hurdles

EUROCONSTRUCT. Briefing on European construction June 2024

EUROCONSTRUCT. Briefing on European construction June 2024

After a difficult four years, the broader UK economy is showing signs of recovery. Yet, the construction sector continues to lag behind, marred by significant challenges. With a general election looming, it is imperative that the next government recognises and addresses these critical issues.

Cause for optimism, room for caution

Following a turbulent four years spurred by the pandemic period and the cost-of-living crisis recent improvements in the UK economy offer a welcome reprieve. The economy clawed its way back from the short-lived recession in 2023H2, with early estimates suggesting GDP grew by 0.6% in the first quarter of this year.

While services inflation remained elevated at 5.7% in May, the overall inflation rate eased to 2%, reaching the Bank of England’s target. We expect this to prompt the Bank of England to begin tentatively cutting rates later in the year. Our central forecast sees two 0.25 basis point cuts, marking a positive development for stalled investment in the construction sector.

Considering this uplift, business and consumer confidence has risen and the UK’s purchasing managers’ indices, which tracks activity in three major sectors (services, manufacturing and construction), all point towards a continued economic recovery.

However, despite broadening optimism, skies ahead remain cloudy for the construction sector amid a sea of budgetary issues and growing concerns surrounding employment. Bucking the first quarter upturn in output, construction activity dipped by 0.9% on the quarter, representing a 0.7% decline on the year. New work output continued to struggle, contracting by a further 1.8%, while renovation activity powered on.

At the business level 399 construction companies, primarily small firms, became insolvent in April. Construction also held the largest share (18%) of company insolvencies across all industries in 2023 at 4,371.

National debt weighs down prospects

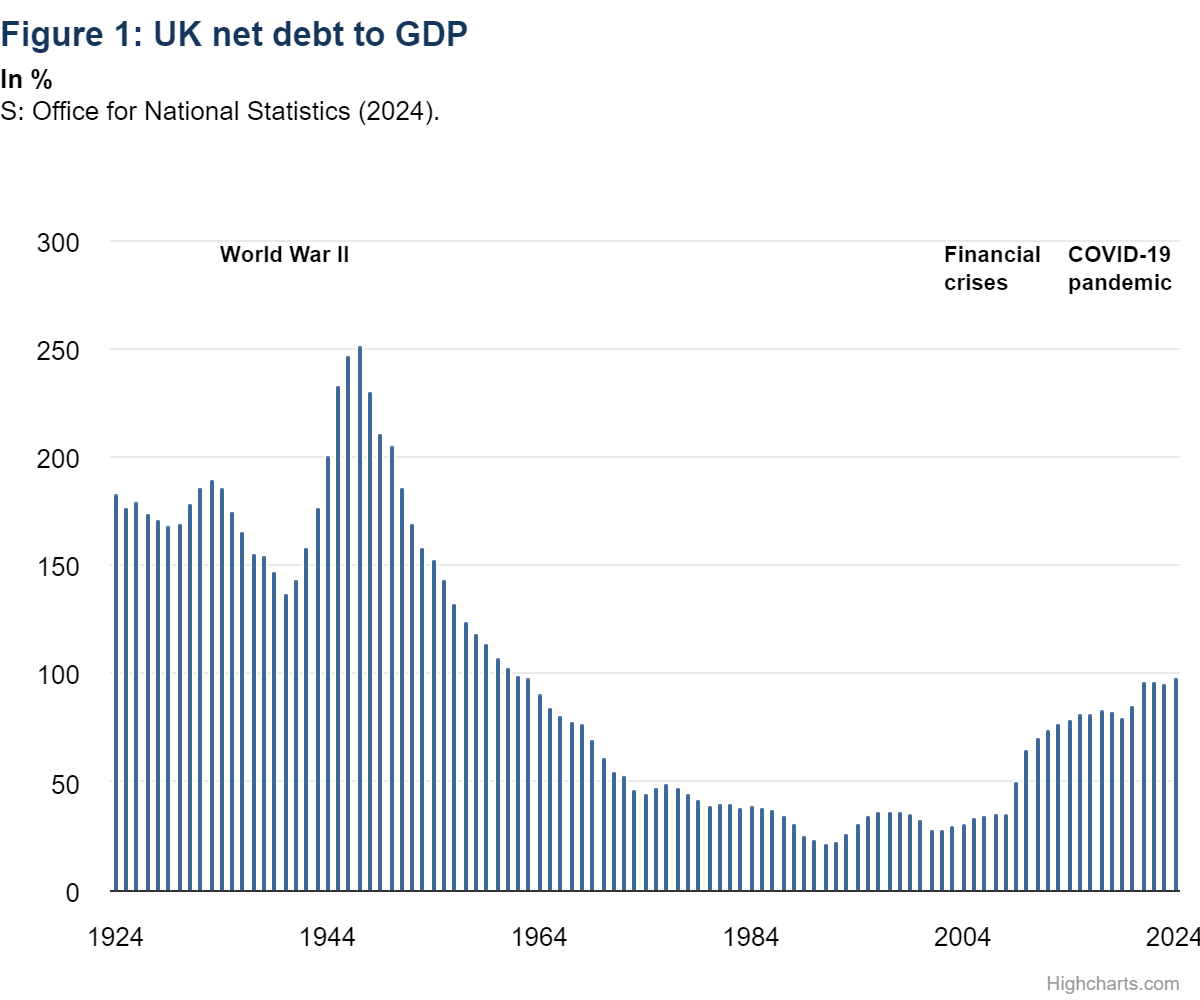

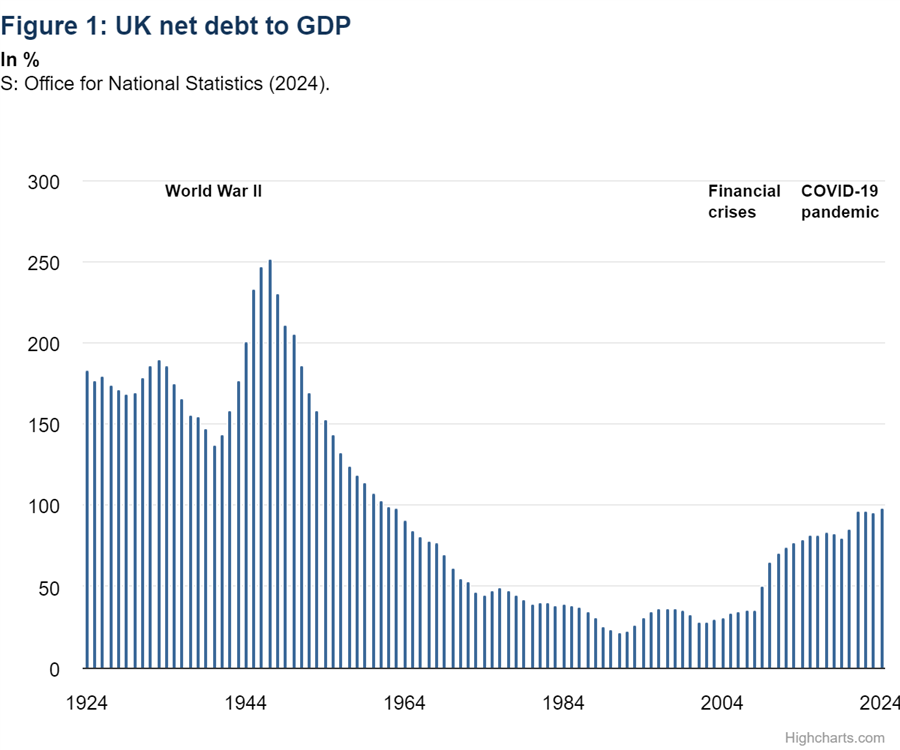

One such obstacle ahead is the UK’s ballooning national debt that reached 97.9% of GDP in April 2024, 2.5 percentage points higher than its position a year earlier and at a high not seen since the early 1960s. Public sector net debt excluding public sector banks (PSND ex) has soared in recent years as a consequence of four years of crisis spending during the pandemic and energy relief schemes to combat the cost-of-living crisis. While this is not disastrous for the country’s prospects given similarly high debt to GDP ratios in other large European economies, it pinpoints the UK’s fiscally constrained position for opportune construction investments moving forwards. A high debt burden typically leads to tepid government spending and results in higher interest rates on government bonds from investors.

Naturally, this makes it more expensive for businesses to borrow money, reducing investment on construction projects and offsetting the gradual stabilisation in materials prices in recent months. It also presents a further roadblock to cautious investors who had stalled project developments through a period of high inflation.

This barrier has risen to the fore considering the upcoming UK general election on July 4th. Both the main parties appear committed to bringing down debt over the course of the parliament. However, there is little detail on how this will be achieved with taxes already at historically high levels and the ailing public sector in need of funding.

With ongoing political focus centred upon healthcare and tax there is little direct support for the construction sector. Labour’s investment to improve the UK’s manufacturing sector and supply chain may support at the margin. This matter extends down from the national level to local authority governments that remain particularly underfunded.

Neither major party have committed to large scale council funding despite English local authorities facing a £6.2bn funding gap according to the Local Government Association. At least six local councils across England, including Nottingham, Birmingham, and Woking have reported bankruptcy since 2021, with a further 20 plus at risk, resulting in many councils’ scaling down construction project plans and reallocating new work funding to repair and maintenance.

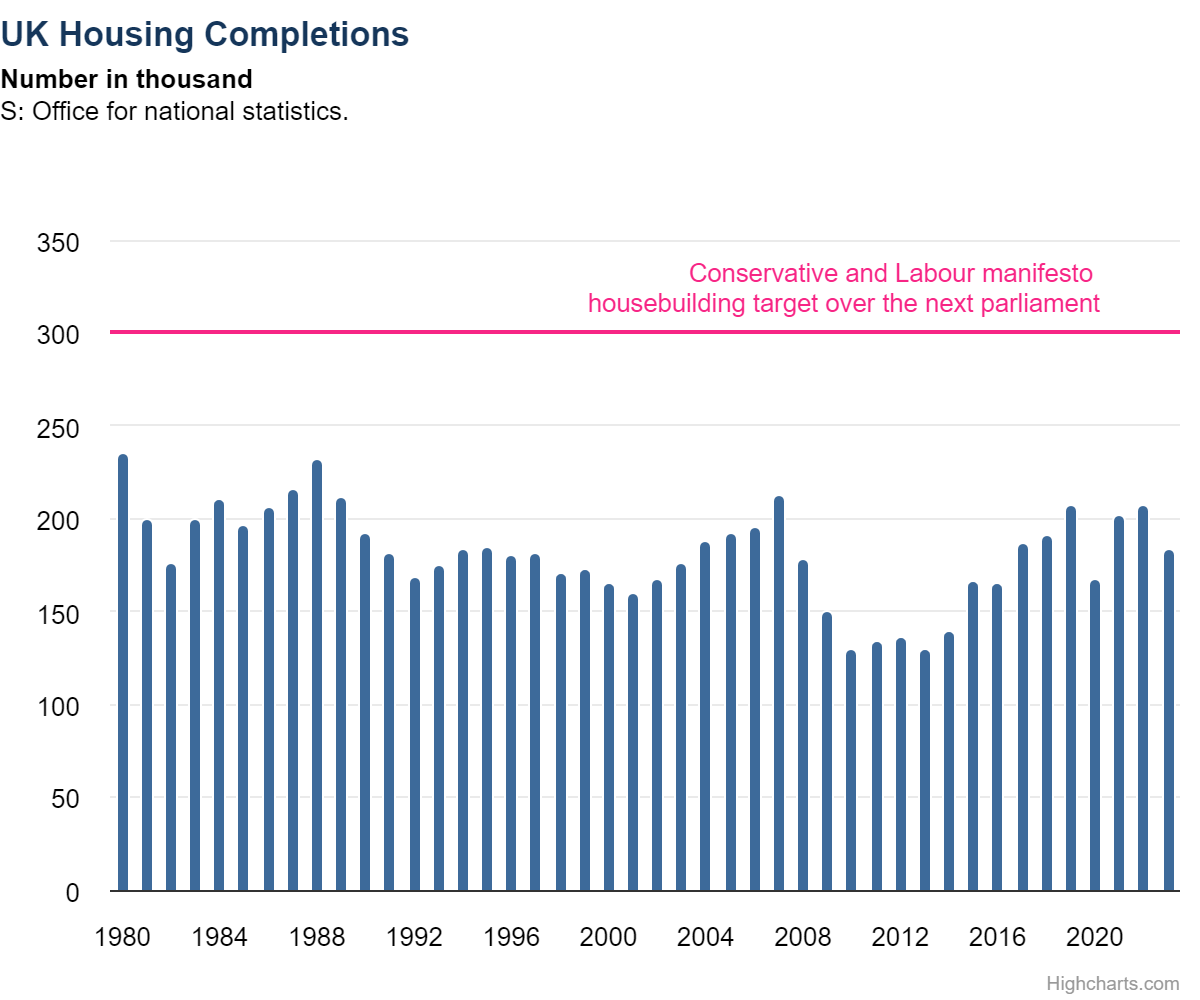

Housing Targets – Ambitious on paper, but foundations built on sand

Similarly to the majority of Europe, the UK is facing a multi-decade underinvestment in the construction of new homes which has led to a sharp squeeze to affordability in recent years. This issue was aggravated by interest rate hikes from December 2021 that has led to roughly 5 million households rolling onto higher mortgage rates.

The associated rise in mortgage repayments has also seen a significant increase in mortgage arrears, to 1.3% in 2024Q1 from 0.9% a year prior according to the Bank of England. Consequently, the matter of the UK producing enough homes has become an increasingly political topic in light of July’s election. Both major parties have announced strikingly similar plans to place a re-injection of interest in the construction of new homes at the forefront of their new government’s policies.

Rishi Sunak, the current Prime Minister and leader of the Conservative party outlined the need for the country to produce 320,000 new homes a year over the five-year parliament. Meanwhile, Sir Kier Starmer, the leader of the opposition Labour Party announced that should his party win, they will aim to build 1.5 million new homes over the next parliament.

On paper this appears as an excellent opportunity for the UK’s residential construction sector, though serious doubts remain as to the feasibility of this target being reached. Current provisional estimates for homes built in 2023 stand at 180,000, down 14% from its 2022 total. A 63% uplift from the 2023 level would be required to reach the lower average target of 300,000 per year from Labour. This still appears unachievable considering the discussed public finances, labour force constraints, housing starts currently in the pipeline, and not least tight planning policies.

Who will build our future?

On a longer-term the UK’s ageing population and elevated economic inactivity are expected to apply further pressure on the fiscal position. The UK has been experiencing steep declines in employment numbers since the loss of EU workers and new visa requirements following Brexit. This issue was exacerbated further by high levels of early retirement among senior workers following the pandemic, a sharp rise in long-term sickness and a shortage of young workers entering the field.

The latest employment data from the Office for National Statistics pointed towards the number of construction workers in the UK falling by 5% relative to before the pandemic (2019Q4), despite high vacancy levels. As a result, there is a growing risk to businesses that worker availability will not be sufficient to meet current building projects, let alone any new ventures set out by whichever government takes office following the election.

Such examples include concerns surrounding the UK’s ambitious plans for modernising infrastructure. Yet this has been marred by the cancellation of the High Speed 2 (HS2) second leg that would have connected London and Birmingham to both Manchester and Leeds. Those also involved in major projects from Hinkley point C nuclear power station to the National Grid have raised the alarm surrounding labour shortages impacting deliveries and extending project delays.

Challenges remain beyond the election

Whichever political party wins the July general election is likely to adopt a UK economy with a brighter outlook than we’ve recently seen, but they would also be managing a construction industry that still faces significant hurdles ahead. Fiscal constraints will continue to place public construction works in a backseat for funding while local governments are expected to continue prioritising repair work. At the same time, the prospects of a new government revitalising construction work for the residential sector presents an exciting opportunity on paper, but realistic concerns have been raised to the feasibility of these plans’ targets. While the necessity and desire might be visible the lack of a workforce to capitalise on the opportunity is a growing concern for the sector’s future, an issue that whoever governs the UK next must take seriously.

Texten är skriven av Lorenzo Rodriguez-Fernandez, makroanalytiker på Experian . Experian är Storbritanniens representant i det europeiska analysnätverket EUROCONSTRUCT. Läs mer om Euroconstruct här eller ta kontakt med oss om du är intresserad av bygg- och anläggningsprognoserna för Europa.