Foreign workers needed to fulfil the labour demand of the Dutch construction sector

Foreign workers needed to fulfil the labour demand of the Dutch construction sector

Briefing on European construction May 2023

Briefing on European construction May 2023

Foreign workers are an important and flexible supply channel of new workers for the Dutch construction industry. With the important tasks around the housing shortage and sustainability, the question is whether EU countries still offer sufficient potential to absorb the required inflow, or whether new regulations are needed to attract professionals from outside the EU.

What is the current size and origin of foreign workers in the Dutch construction industry?

In 2020, 56,000 foreign workers were engaged in construction in the Netherlands, 15,000 more than in 2017. There has been an acceleration in growth compared to previous years. The growth occurred mainly in 2018 and 2019, due to the COVID-19 pandemic in 2020 there was a decline in temporary personnel.

Of the total number of foreign workers and self-employed in Dutch construction in 2020, 60% were from Central and Eastern European countries. Poland retains the leading share in this at 35%.

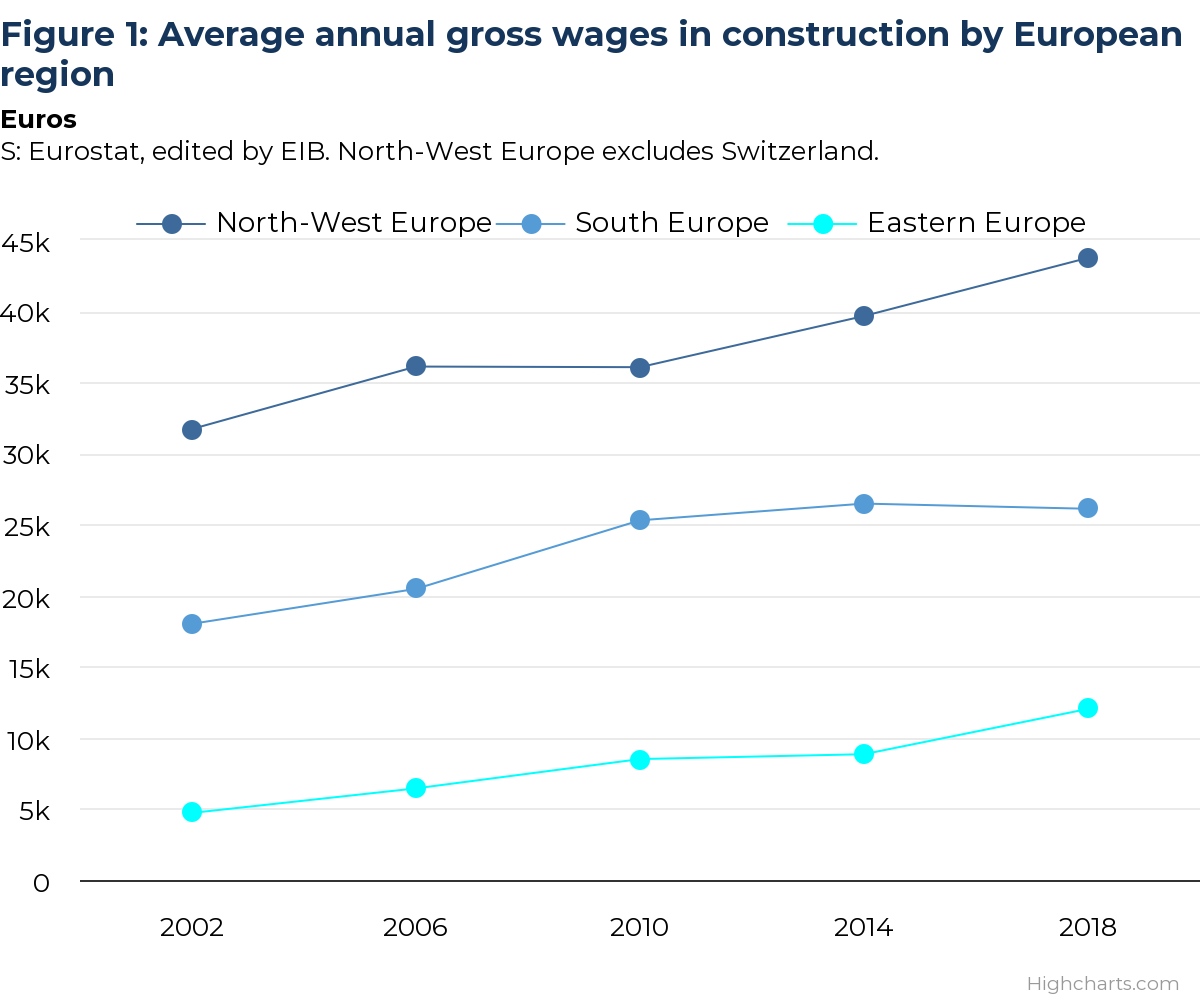

An important motive for a foreign worker to come and work in Dutch construction is the wage difference between the Netherlands and the country of origin. The wages in Eastern Europe have more than doubled between 2002 and 2018, but the wage gap with North-West Europe is still significant (figure 1). Within North-West Europe, the Netherlands has relatively high gross wages (€ 50,000) which makes a favourable competitive position for attracting foreign workers.

How does the demand for foreign labour in Dutch construction develop?

Based on expected employment growth and the number of people leaving the construction industry permanently because of retirement or disability, the annual required inflow of new workforce is determined. Also the proportions of the various ways of workforce inflow is determined: graduates from construction education programs, foreign workers and inflow from other industries. To answer the question how the demand for foreign labour in the Dutch construction develops we differentiate between two scenarios: the base scenario and an ambitious scenario.

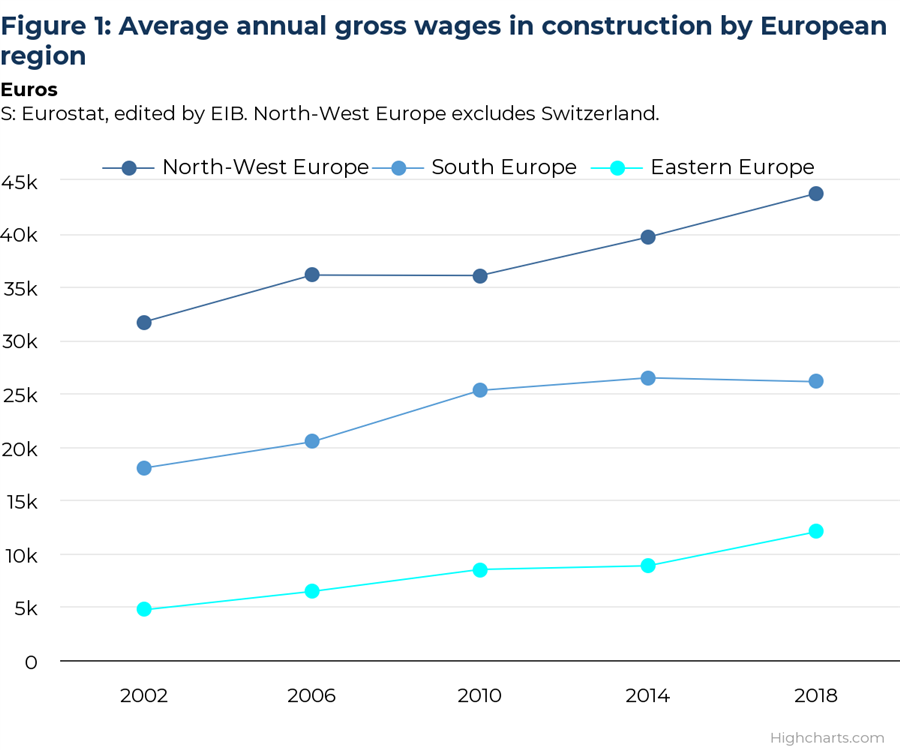

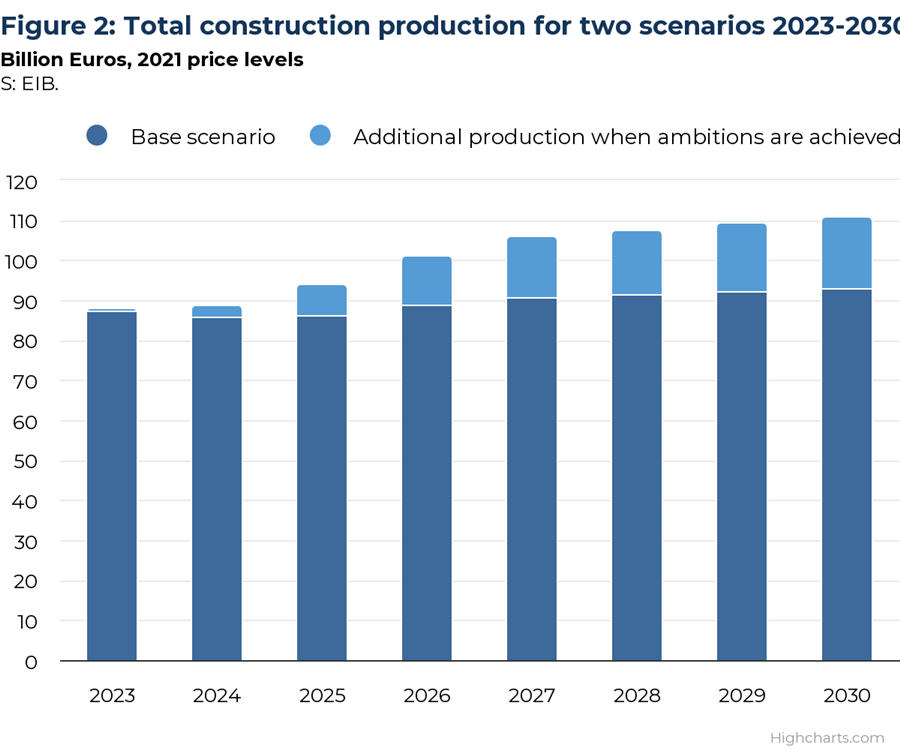

In the base scenario we assume a short-term decline in construction output due to the worsened economic situation due to the war in Ukraine. In the medium term (2025-2027) production increases by an average of 2% per year and in the long term (2028-2030) 0,5% per year (figure 2).

In the ambitious scenario we explore the maximum need for foreign labour inflow and therefore assume the accomplishment of the ambitious plans of the Dutch government: completing 100,000 new homes per year within a few years and making 1,500,000 homes natural gas-free by 2030, in addition to intensifications around insulation and installation activities. The production in this scenario increases by an average of 5% per year in the medium term and 1,5% in the long term.

In the base scenario there is very little demand for foreign workers in the short term. The supply of workers from construction education is more than sufficient to meet the low inflow requirement in 2023 and 2024. In the medium term (2025-2027) 1,500 foreign workers are needed yearly to meet the required inflow. This seems easily achievable in light of the growth realised in 2018 and 2019. After 2027 the inflow from construction education is more than sufficient to meet the needed inflow and no additional foreign workers are needed.

In the ambitious scenario the inflow requirement is much higher due to a higher production level. The inflow from construction education and other industries will not be sufficient to meet the demand. Especially in the medium term the inflow requirement from foreign workers will be high: from 2025-2027 around 10,000 per year. In the long term (2028-2030) the demand for foreign inflow will decline to 3,400 per year.

Do the current EU countries offer sufficient potential for Dutch demand or is additional supply from non-EU countries needed?

The required inflow of foreign labour until 2030 seems well realisable for both scenarios. The task lies mainly in the medium term. As stated before, in the base scenario the required inflow of foreign workers is in the medium term 1,500 per year. This is significantly lower than what was realised in years 2018 and 2019. In the years 2018 and 2019, the number of foreign workers increased by an average of 10,000 per year. In the long term (2028-2030) the required inflow can be realised entirely from Dutch education programs, which means the inflow of foreign workers will not be needed.

In the scenario where the high ambitions of the Dutch government will be realised, the pressure on the construction labour market is significantly greater. In the medium term (2025-2027), this scenario requires an additional inflow of 10,000 foreign workers annually. This is the same level of foreign workers as in 2018 and 2019. Due to the fact that the COVID-19 pandemic has ended (travel restrictions) and employment agencies indicate that supply of foreign workers is recovering strongly, the required inflow of 10,000 foreign workers seems well realisable.

To meet the required inflow of construction workers in the ambitious variant in the medium term an additional 7,000 workers from other industries should enter the construction sector yearly (next to the inflow from construction education and foreign workers). In the years 2017-2019 the average inflow from other industries was well above this (12,500 workers per year). In the current situation, however, many other Dutch industries are also suffering from the tight labour market. Consequently, the required inflow from other industries in the medium term is high under these circumstances. It is possible, but it will require great efforts by the construction sector.

In the end, the demand for foreign workers in the Dutch construction sector depends on economic and policy developments in the coming years. The developments of the construction sector in the Netherlands and the rest of Europe in times of rising prices and interest rates will be the topic of the upcoming Euroconstruct conference in Amsterdam (8-9 June). More information and registration can be found here.

Texten är skriven av Vera Uunk, expert på den nederländska bygg- och anläggningsmarknaden vid EIB - Economisch Instituut vor der Bouw. EIB ingår tillsammans med Prognoscentret i det europeiska analysnätverket Euroconstruct som tar fram prognoser för nitton europeiska bygg- och anläggningsmarknader två gånger per år. Kontakta oss för mer information om Euroconstructs prognoser och rapporter.